When it comes to home equity loans vs HELOC, the choices can be overwhelming. Let’s dive into the details to see which option best suits your financial needs.

This comparison will shed light on the pros and cons of each, helping you make an informed decision for your home financing.

Exploring the Benefits of Solar Energy

Solar energy is a renewable and sustainable source of power that offers numerous benefits to both the environment and homeowners. By harnessing the power of the sun, solar energy systems can significantly reduce carbon emissions and dependence on fossil fuels.

Environmental Advantages of Using Solar Energy

- Solar energy produces clean electricity without releasing harmful pollutants into the atmosphere, helping to combat climate change.

- By reducing the reliance on traditional sources of energy like coal and natural gas, solar energy contributes to a healthier environment and cleaner air quality.

Potential Cost Savings Associated with Solar Energy Systems

- Installing solar panels can lead to long-term cost savings on electricity bills, as homeowners generate their own power from the sun.

- With advancements in technology and decreasing installation costs, the return on investment for solar energy systems has become more attractive over time.

Government Incentives and Rebates for Installing Solar Panels

- Federal tax credits are available for homeowners who install solar panels, providing a financial incentive to go solar.

- Many states and local governments also offer rebates and incentives for solar energy systems, further reducing the upfront costs of installation.

Home Equity Loans

When considering a home equity loan, borrowers often have to decide between fixed and variable rates. Each option comes with its own set of advantages and disadvantages, depending on individual financial goals and risk tolerance.

Fixed-rate Home Equity Loans

Fixed-rate home equity loans offer predictability in monthly payments, making budgeting easier for borrowers. Additionally, they provide protection against interest rate hikes, ensuring that the rate remains constant throughout the loan term.

- Interest rates do not change over time, providing stability in payments.

- Borrowers can accurately plan and budget for monthly expenses.

- Protection against rising interest rates offers peace of mind.

Variable-rate Home Equity Loans

Variable-rate home equity loans start with lower initial rates that can adjust periodically based on market conditions. These loans may be advantageous in a declining interest rate environment, potentially leading to lower overall costs for borrowers.

- Initial lower rates may result in lower initial costs for borrowers.

- Rates can fluctuate over time, potentially leading to increased payments in a rising rate environment.

- Borrowers willing to take on some risk may benefit from potential interest rate decreases.

Choosing the Right Loan

Fixed-rate home equity loans are ideal for borrowers seeking stability and predictability in their payments. On the other hand, variable-rate loans may be suitable for those willing to take on some risk for the potential of lower initial costs.

| Feature | Fixed-rate Home Equity Loans | Variable-rate Home Equity Loans |

|---|---|---|

| Interest Rate Fluctuation | Stable, does not change over time | Can fluctuate based on market conditions |

| Payment Predictability | Monthly payments remain constant | Payments can vary over time |

| Overall Cost Over Time | Potentially higher initial costs | Potentially lower initial costs |

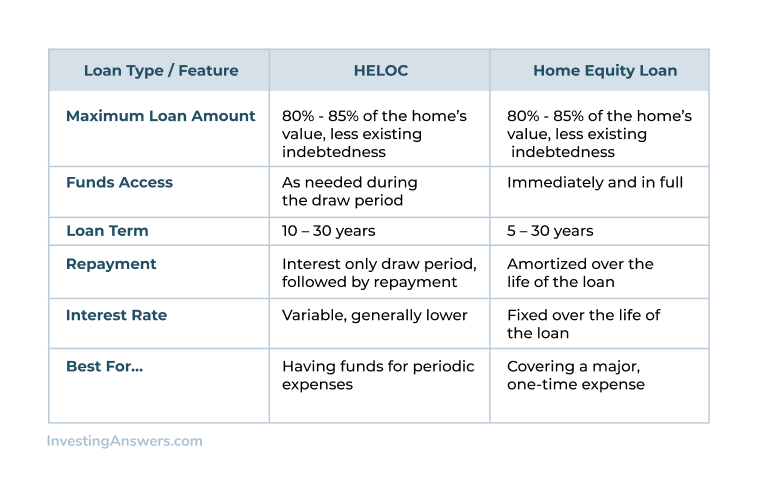

HELOCs

Home Equity Line of Credit (HELOC) offers homeowners a flexible way to access funds based on the equity in their homes. Unlike a traditional home equity loan, a HELOC functions as a revolving line of credit, allowing homeowners to borrow as needed.

Line of Credit Flexibility

A HELOC operates similar to a credit card, where homeowners can access funds up to a certain limit determined by the equity in their home. They can borrow and repay multiple times, making it a convenient option for ongoing expenses or projects.

- Homeowners can access funds through a HELOC by simply writing a check, using a credit card linked to the account, or transferring funds online.

- The interest rates on a HELOC are typically lower than other forms of credit, making it a cost-effective way to borrow money.

- Examples of how homeowners can use the flexibility of a HELOC include funding home renovations, consolidating higher interest debt, or covering unexpected expenses.

Qualification Requirements for Home Equity Loans and HELOCs

When looking to tap into the equity of your home, it’s important to understand the qualification requirements for both home equity loans and HELOCs. These requirements can vary depending on the lender and the amount of equity you have in your home.

Typical Eligibility Criteria for Home Equity Loans

- A minimum credit score of around 620 to 640.

- A debt-to-income ratio of no more than 43%.

- An equity stake in your home of at least 15% to 20%.

- Stable income and employment history.

- Clean credit history with no recent bankruptcies or foreclosures.

Comparison of Qualification Requirements for HELOCs and Home Equity Loans

- HELOCs typically have lower credit score requirements, often around 680.

- HELOCs may have a higher debt-to-income ratio allowance, up to 50% in some cases.

- HELOCs may require a lower equity stake, sometimes as low as 10%.

- Both may require a stable income and employment history.

Factors Impacting Qualification for Home Equity Loans and HELOCs

- Fluctuations in home values can affect the amount of equity available to borrow against.

- Changes in credit score or financial situation can impact eligibility for both types of loans.

- Lenders may have specific requirements or restrictions based on their own policies.

- Economic factors, such as interest rates or housing market conditions, can also play a role.

Loan Amounts and Disbursement Methods

When it comes to personal loans, the loan amount you can qualify for and the disbursement methods available can vary based on several factors.

Factors Considered for Loan Amounts

- Your income and employment status play a significant role in determining the loan amount you qualify for. Lenders typically look for a stable source of income to ensure you can repay the loan.

- Your credit score also influences the loan amount. A higher credit score usually means you can qualify for a larger loan amount at a lower interest rate.

- Your debt-to-income ratio is another important factor. Lenders consider how much of your income goes towards paying off existing debts before determining the loan amount.

Fixed vs. Variable Interest Rates

- A fixed interest rate remains the same throughout the loan term, providing predictability in monthly payments. In contrast, a variable interest rate can fluctuate based on market conditions, leading to potential changes in your monthly payment amount.

- With a fixed interest rate, you can budget more effectively as your payments will remain constant. However, a variable interest rate may offer lower initial rates but comes with the risk of increasing over time.

Collateral for Personal Loans

- Collateral can be used to secure a personal loan and reduce the lender’s risk. Common types of collateral include real estate, vehicles, savings accounts, or valuable assets like jewelry or art.

- If you fail to repay the loan, the lender can seize the collateral to recover their funds. Using collateral can sometimes result in a lower interest rate or a higher loan amount.

Repayment Term Options

- Choosing a fixed repayment term means you have a set timeline to repay the loan, offering clarity and structure in your financial planning. This option is ideal if you prefer consistent monthly payments.

- Opting for a flexible repayment term allows you to adjust your monthly payments based on your financial situation. While it offers more flexibility, it can result in a longer repayment period and potentially higher overall interest costs.

Impact of Credit Score

- Your credit score plays a crucial role in the approval process for personal loans. A higher credit score indicates a lower credit risk, making you more attractive to lenders and potentially qualifying you for larger loan amounts and better interest rates.

- A lower credit score, on the other hand, can limit your borrowing options, leading to higher interest rates or smaller loan amounts. Improving your credit score before applying for a personal loan can increase your chances of approval and better loan terms.

Repayment Terms and Options

Repayment terms and options are crucial aspects to consider when taking out a home equity loan or HELOC. Understanding the different repayment structures and strategies can help homeowners manage their finances effectively and avoid potential pitfalls.

Typical Repayment Terms for Home Equity Loans

- Home equity loans typically come with fixed monthly payments over a set term, usually ranging from 5 to 30 years.

- Interest rates are fixed, providing predictability in monthly payments.

- Homeowners can choose to pay off the loan early without facing prepayment penalties.

Various Repayment Options for HELOCs

- HELOCs offer more flexibility in repayment, allowing homeowners to borrow and repay funds as needed during the draw period.

- Monthly payments during the draw period may consist of interest-only payments or payments towards both principal and interest.

- After the draw period, homeowners enter the repayment period, where they must repay the remaining balance over a set term.

Managing Repayment Effectively

- Homeowners can set up automatic payments for both home equity loans and HELOCs to ensure timely repayments and avoid late fees.

- Monitoring spending habits and creating a budget can help homeowners allocate funds towards loan repayments effectively.

- Exploring refinancing options or debt consolidation can help manage repayments if financial circumstances change.

Comparison of Repayment Schedules

- Fixed-rate home equity loans have consistent monthly payments, making budgeting easier for homeowners.

- Variable-rate HELOCs may have fluctuating monthly payments based on changes in the interest rate, requiring homeowners to budget accordingly.

Setting Up Automatic Payments

- Contact your lender to set up automatic payments for your home equity loan by linking your bank account for seamless transactions.

- Ensure that there are sufficient funds in your account to cover the monthly payments to avoid overdraft fees.

- Review your payment schedule regularly to make adjustments if needed and stay on track with repayments.

Consequences of Missing Repayments

- Missing repayments on a home equity loan or HELOC can result in late fees, increased interest rates, and damage to your credit score.

- Repeated missed payments may lead to foreclosure or repossession of your home, putting your homeownership at risk.

- It is essential to communicate with your lender if you encounter financial difficulties to explore options and avoid defaulting on the loan.

Customized Repayment Strategy

- Create a personalized repayment plan based on your financial goals, including setting aside extra funds for additional payments towards the principal.

- Explore bi-weekly payment options or making lump-sum payments to reduce the overall interest paid and shorten the loan term.

- Consult with a financial advisor to tailor a repayment strategy that aligns with your financial situation and helps you achieve your long-term objectives.

Interest Rates and Costs

When it comes to home equity loans and HELOCs, understanding the interest rates and costs involved is crucial for homeowners looking to tap into their home’s equity.

Interest Rates Comparison

- Home Equity Loans: Typically, home equity loans come with fixed interest rates, providing certainty in monthly payments over the loan term.

- HELOCs: HELOCs usually have variable interest rates, which means monthly payments can fluctuate based on market conditions.

Costs Involved

- Home Equity Loans: Closing costs for home equity loans can range from 2% to 5% of the loan amount, which may include appraisal fees, origination fees, and other charges.

- HELOCs: HELOCs may have lower upfront costs compared to home equity loans, but borrowers may encounter annual fees, transaction fees, and early closure fees.

Minimizing Interest Costs and Fees

- Shop Around: Compare offers from different lenders to find the best interest rates and lowest fees.

- Consider Fixed Rates: If you prefer predictability in payments, opt for a home equity loan with a fixed interest rate.

- Use Funds Wisely: Borrow only what you need to avoid paying unnecessary interest on a larger loan amount.

- Pay on Time: Timely payments can help maintain a good credit score and potentially qualify you for lower interest rates in the future.

Tax Deductibility of Home Equity Loans and HELOCs

When it comes to home equity loans and HELOCs, tax deductibility is an important aspect to consider. Interest payments on these loans may have tax implications, and it’s essential to understand how they can potentially benefit you financially.

Tax Implications of Interest Payments on Home Equity Loans

Interest payments on a home equity loan may be tax-deductible if the loan is used to improve your primary residence. This means that if you use the funds to make renovations or repairs that increase the value of your home, the interest you pay on the loan may be eligible for a tax deduction.

Criteria for Tax Deductibility of HELOC Interest

For interest paid on a HELOC to be tax-deductible, the funds must be used to buy, build, or substantially improve the home that secures the loan. The IRS has specific criteria that determine whether the interest is eligible for deduction, so it’s crucial to keep detailed records of how you use the HELOC funds.

Comparison of Tax Benefits between Home Equity Loans and HELOCs

Both home equity loans and HELOCs offer potential tax benefits through deductibility of interest payments. However, the specific criteria for eligibility may vary between the two types of loans. Home equity loans are typically used for a lump-sum amount, while HELOCs provide a revolving line of credit, which may impact the tax benefits available.

Steps to Maximize Tax Benefits from Home Equity Loans and HELOCs

To ensure you can claim the maximum tax benefits from your home equity loan or HELOC, it’s essential to keep detailed records of how you use the funds. Make sure to consult with a tax professional to understand the specific criteria for deductibility and take advantage of any potential tax savings.

Comparison Table of Tax Deductibility

| Aspect | Home Equity Loans | HELOCs |

|---|---|---|

| Eligible Use | Improving primary residence | Buying, building, or improving home |

| Loan Type | Lump-sum | Revolving line of credit |

| Documentation | Record of home improvement expenses | Detailed use of funds documentation |

Risk Factors and Considerations

When considering taking out a home equity loan or using a HELOC, it’s important to understand the potential risks involved. These financial products are secured by your home, so failing to repay them could result in the loss of your property. Let’s explore some key risk factors and considerations to keep in mind.

Potential Risks of Home Equity Loans and HELOCs

- Defaulting on Payments: If you are unable to make timely payments on your home equity loan or HELOC, you risk facing foreclosure and losing your home.

- Variable Interest Rates: HELOCs often come with variable interest rates, which means your monthly payments can fluctuate based on market conditions.

- Additional Debt Burden: Taking out a home equity loan or HELOC increases your overall debt load, which could strain your finances if unexpected expenses arise.

Strategies for Mitigating Risks

- Assess Your Financial Situation: Before taking out a home equity loan or HELOC, carefully evaluate your ability to repay the loan based on your current income and expenses.

- Consider Fixed-Rate Options: Opting for a fixed-rate home equity loan can provide stability in your monthly payments, eliminating the risk of interest rate hikes.

- Use Funds Wisely: Avoid using the funds from a home equity loan or HELOC for unnecessary expenses and instead focus on investments that can increase your home’s value or generate income.

Impact on Home Equity and Property Ownership

When considering home equity loans and HELOCs, it’s important to understand how these financial tools can impact a homeowner’s equity in their property. Leveraging home equity for these loans can have both short-term and long-term implications on property ownership.

Effect on Home Equity

- By taking out a home equity loan or HELOC, homeowners are essentially borrowing against the value of their property. This can reduce the amount of equity they have in their home.

- As the loan is paid off, the homeowner’s equity may increase again. However, it’s crucial to consider the impact of interest rates and repayment terms on the overall equity position.

Implications of Leveraging Home Equity

- Using home equity for loans can provide access to funds for various purposes such as home improvements, debt consolidation, or other financial needs.

- However, tapping into home equity also means taking on additional debt secured by the property, which can put the homeowner at risk of foreclosure if they are unable to make payments.

Long-Term Property Ownership Impact

- Home equity loans and HELOCs can impact long-term property ownership by influencing the overall financial health of the homeowner.

- If the loans are managed responsibly and payments are made on time, they can be a valuable financial tool. On the other hand, mismanagement can lead to financial strain and potential loss of the property.

Application and Approval Process

When it comes to applying for a home equity loan or a HELOC, understanding the process is crucial to ensure a smooth and successful approval. Here we will detail the steps involved in applying for these loans and provide tips to streamline the process.

Home Equity Loan Application Process

- Gather necessary financial documents such as income statements, tax returns, and proof of homeowners insurance.

- Complete the application form provided by the lender, ensuring all information is accurate and up-to-date.

- Submit the required documentation along with the application form to the lender for review.

- Wait for the lender to assess your application, which may involve a credit check and appraisal of your property.

- Once approved, review the terms and conditions of the loan and sign the agreement to proceed with the disbursement of funds.

HELOC Approval Timeline

- The approval timeline for a HELOC can vary depending on the lender and individual circumstances.

- Typically, the processing duration for a HELOC can range from a few days to a few weeks.

- Key factors that can affect the speed of approval include the completeness of your application, your credit score, and the current workload of the lender.

Tips for Streamlining the Process

- Maintain a good credit score to increase your chances of approval and secure favorable terms.

- Prepare a detailed budget plan outlining how you intend to use the funds from the loan or HELOC.

- Promptly respond to any requests for additional information from the lender to avoid delays in the approval process.

Market Trends and Interest Rate Environment

Market trends play a crucial role in determining the interest rates for home equity loans. By analyzing historical data and identifying key factors that influence rate changes, homeowners can better understand how to navigate the interest rate environment.

Impact of Market Trends on Interest Rates

- Market trends such as economic indicators, inflation rates, and Federal Reserve policies can all affect interest rates for home equity loans.

- Changes in the housing market, unemployment rates, and overall economic conditions can also impact interest rates.

Current Interest Rate Environment

- The current interest rate environment for HELOCs is influenced by factors like the prime rate, borrower’s creditworthiness, and loan-to-value ratios.

- Comparisons with fixed-rate mortgages show that HELOCs typically have variable interest rates, which can fluctuate over time.

Navigating Changing Interest Rates

- Homeowners can strategize to secure favorable rates by monitoring market trends and timing their loan applications accordingly.

- Consider refinancing options or locking in rates during periods of low interest rates to mitigate the impact of rate fluctuations.

Interest Rate Trends in the Past Five Years

| Year | Interest Rate (%) |

|---|---|

| 2017 | 4.2 |

| 2018 | 5.1 |

| 2019 | 3.8 |

| 2020 | 4.5 |

| 2021 | 3.6 |

Experts suggest that homeowners should closely monitor market trends and consult with financial advisors to make informed decisions about home equity loans.

Home Improvement Projects and Financing

When it comes to financing home improvement projects, homeowners have options like home equity loans and HELOCs to consider. These can provide the necessary funds to renovate or upgrade their homes, increasing property value and enhancing the living space.

Using a Home Equity Loan for Renovation Projects

Homeowners can use a home equity loan to fund major renovation projects like kitchen remodels, bathroom upgrades, or adding a new room to their home. These loans typically offer a lump sum payment upfront, allowing for planned expenses and fixed repayment terms.

- Renovating a kitchen with modern appliances and fixtures.

- Upgrading bathrooms with new tiles, vanities, and fixtures.

- Adding a backyard deck or patio for outdoor entertaining.

HELOC as a Flexible Financing Option for Ongoing Improvements

A HELOC can be a great choice for ongoing home improvement needs, as it functions like a credit card with a revolving line of credit. Homeowners can draw funds as needed, making it a flexible option for projects that have varying costs or timelines.

- Continuous upgrades like landscaping improvements or exterior painting.

- Remodeling projects that require multiple phases or stages.

- Emergency repairs or maintenance work around the house.

Maximizing the Value of Home Equity Loans and HELOCs for Home Upgrades

To get the most out of these financing options when investing in home upgrades, homeowners should focus on projects that increase property value, improve energy efficiency, or enhance the overall livability of the home. Additionally, comparing interest rates and repayment terms can help in making an informed decision.

Differences in Interest Rates and Repayment Terms

Home equity loans typically have fixed interest rates and repayment terms, making them predictable and stable for budgeting purposes. On the other hand, HELOCs offer variable rates and flexible repayment schedules, which can be advantageous in certain situations.

Eligibility Criteria for Home Equity Loans and HELOCs

When applying for a home equity loan or a HELOC, homeowners need to meet certain eligibility criteria such as having sufficient equity in their property, a good credit score, and a stable income. Lenders may also consider other factors like debt-to-income ratio and loan-to-value ratio.

Risks of Using Home Equity for Renovation Projects

Using home equity as a financing option for renovation projects comes with risks, such as the potential to overextend financially, default on payments, or decrease home equity in case of property value depreciation. It’s essential to weigh these risks before proceeding with a loan.

Steps for Applying for Home Equity Loans and HELOCs

The application process for a home equity loan or a HELOC typically involves providing documentation such as income verification, property appraisal, credit history, and debt obligations. Lenders assess the financial profile of the homeowner to determine loan approval.

Pros and Cons of Using Home Equity Loan vs. HELOC for Home Improvement Projects

| Home Equity Loan | HELOC |

|---|---|

| Fixed interest rates and predictable payments | Variable rates and flexible draw period |

| Lump sum payment for planned expenses | Revolving line of credit for ongoing needs |

| Suitable for one-time projects with fixed costs | Ideal for projects with varying costs or timelines |

Debt Consolidation Strategies

When it comes to managing multiple high-interest debts, homeowners have the option to utilize their home equity to consolidate these debts into a single, more manageable loan. This can help simplify their finances and potentially save money on interest payments in the long run.

Using Home Equity Loans for Debt Consolidation

Homeowners can use a home equity loan to consolidate high-interest debt by borrowing against the equity in their home. This lump sum loan allows them to pay off existing debts, such as credit card balances or personal loans, with a lower interest rate and fixed monthly payments over a set period of time.

Advantages and Potential Pitfalls of Using a HELOC for Debt Consolidation

While a Home Equity Line of Credit (HELOC) offers flexibility in borrowing against the equity in a home, it also poses risks if not managed properly. HELOCs have variable interest rates that can fluctuate over time, potentially leading to higher monthly payments. However, homeowners can benefit from the ability to access funds as needed and only pay interest on the amount borrowed.

Examples of Effective Debt Consolidation with Home Equity Loans

- Consolidating multiple credit card balances into a single home equity loan with a lower interest rate.

- Using a home equity loan to pay off a high-interest personal loan, reducing overall interest costs.

- Combining various debts, such as medical bills or student loans, into one manageable payment through a home equity loan.

Future Outlook and Considerations

The landscape of home equity borrowing, including home equity loans and HELOCs, is constantly evolving. Understanding the future outlook and considerations can help homeowners make informed decisions about leveraging their home equity for financial needs.

Trends in Home Equity Borrowing

- Increasing popularity of home equity loans and HELOCs as homeowners look for ways to fund home improvements, consolidate debt, or cover major expenses.

- Growing acceptance of these borrowing options as viable alternatives to traditional loans due to lower interest rates and potential tax benefits.

- Rise in online platforms offering streamlined application processes for home equity loans and HELOCs, making them more accessible to a wider range of homeowners.

Considerations for Homeowners

- Interest rate fluctuations in the market can impact the cost of borrowing with home equity loans and HELOCs, making it essential for homeowners to monitor rates closely.

- Changes in property values can affect the amount of equity available for borrowing, prompting homeowners to stay informed about the real estate market in their area.

- Regulatory changes or economic factors may influence the availability and terms of home equity loans and HELOCs, requiring homeowners to stay updated on industry developments.

Future Implications

- Continued innovation in the home equity borrowing sector may lead to more flexible loan products and terms tailored to the needs of different homeowner demographics.

- Advancements in technology could further streamline the application and approval process for home equity loans and HELOCs, enhancing convenience for borrowers.

- Increased awareness of the benefits and risks associated with home equity borrowing may empower homeowners to make sound financial decisions that align with their long-term goals.

Closing Notes

In conclusion, weighing the advantages of home equity loans against the flexibility of HELOCs is crucial in making a smart financial decision for your future investments.